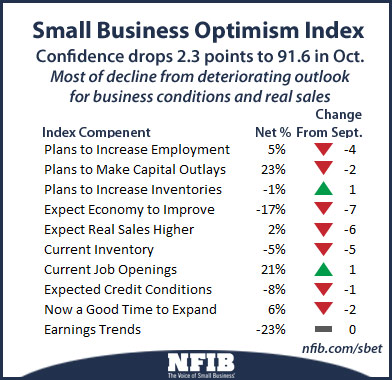

Fall arrived literally this month, as small business optimism dropped from 93.9 to 91.6, largely due to a precipitous decline in hiring plans and expectations for future small-business conditions. The latest NFIB Small Business Index found that seven of its 10 Index components turned negative, falling a total of 27 percentage points. The stalemate in early October over funding the government as well as the failed “launch” of the Obamacare website left 68 percent of owners feeling that the current period is a bad time to expand; 37 percent of those owners identified the political climate in Washington as the culprit – a record high level.

“Washington paralysis is never good news for the economy, so it was no surprise that while politicians were arguing over whether or not the government should remain fully operational, small-business optimism measures deteriorated,” said NFIB chief economist Bill Dunkelberg. “Small employers are not fooled by headlines announcing record high stock market indices; everyday they live the economic realities of overregulation, increased taxes, weak sales and a government without any direction or plan for the future. The average value of the Index since the recovery started is 91 – 8 points below the 35-year average through 2007 and well below readings typically experienced in a recovery. The new budget deadline of January 15, 2014 is approaching quickly and Congress continues to wrangle over the disastrous healthcare law and little else. We shouldn’t expect skies to turn blue anytime soon.”

The NFIB Optimism Index provides an excellent opportunity to examine the impact of major events with “before and after” interviews from small-business owners. In the case of the government shutdown, the majority of the September survey responses were received a week before the end of the month; two-thirds of the 1,940 October surveys were received and recorded by October 20, the height of the shut-down debate. Thus, the two monthly surveys provide a very good “before and after” analysis. Late in September, the likelihood of a shutdown grew, but the September interviews were also mostly completed and processed well before the end of the month.

A review of the October indicators is as follows:

- Job Creation. Job creation was up in October. NFIB owners increased employment by an average of 0.11 workers per firm in October after September’s decline.

- Hard to Fill Job Openings. Twenty-one percent of all owners reported job openings they could not fill in the current period (up 1 point), and 15 percent reported using temporary workers, up 1 point from September. Most of the jobs “created” will likely be dominated by part-time workers as owners hedge their hiring while they try to fathom the health care law regulations and penalties.

- Sales. The net percent of all owners reporting higher nominal sales in the past three months compared to the prior three months dropped 2 points to a negative 8 percent. The net percent of owners expecting higher real sales volumes fell 6 points to 2 percent of all owners.

- Earnings and Wages. Earnings trends did not improve in October, remaining at a negative 23 percent. Two percent of owners reported reduced worker compensation and 18 percent reported raising compensation, yielding a net 16 percent reporting higher worker compensation (down 1 point). A net 10 percent plan to raise compensation in the coming months, down 3 points. Overall, the compensation picture remained at the better end of experience in this recovery, but historically weak for periods of economic growth and recovery.

- Credit Markets. Credit continues to be a non-issue for small employers, 6 percent of whom say that all their credit needs were not met in October, unchanged from the previous month. Twenty-eight percent of owners surveyed reported all credit needs met, and 53 percent explicitly said they did not want a loan.

- Capital Outlays. In October, the frequency of reported capital outlays over the past six months rose 2 points to 57 percent. The percent of owners planning capital outlays in the next three to six months fell 2 points to 23 percent.

- Good Time to Expand. Only 6 percent of owners characterized the current period as a good time to expand (down 2 points from September). The net percent of owners expecting better business conditions in six months was a net negative 17 percent, 7 points worse than September and 15 points worse than August.

- Inventories.The pace of inventory reduction continued in September, with a net negative 6 percent of all owners reporting growth in inventories, up 1 point from September. For all firms, a net negative 5 percent (a 5 point drop) reported stocks too low, the lowest reading since 2011. Plans to add to inventories increased 1 point for a net negative 1 percent.

- Inflation. Fourteen (14) percent of the NFIB owners surveyed reported reducing their average selling prices in the past three months (unchanged), and 16 percent reported price increases (up 2 points). The net percent of owners raising average selling prices was 5 percent, up 4 points. As for prospective price increases, a net 18 percent plan price hikes, down 1 point. Twenty percent plan on raising average prices in the next few months (unchanged), and 3 percent plan reductions (up 1 point).

The report is based on the responses of 1,940 randomly sampled small businesses in NFIB’s membership, surveyed throughout the month of October.

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs

Tags: Small Business